{kind=link}

Key Points

- Lightspeed is growing its client base and penetration of service, delivering leverage and cash flow to repurchase shares.

- Grab is a super-app dominating eCommerce in Southeast Asia, and it is undervalued.

- Katapult gains traction and grows at a double-digit pace.

- 5 stocks we like better than Grab

Tech stocks offer the largest gains for investors because the opportunity for growth is immense. Often started from nothing, microcap tech stocks can blossom into market-leading names, with Alphabet NASDAQ: GOOGL, Apple NASDAQ: AAPL, and Microsoft NASDAQ: MSFT as prime examples. This article examines three hot-tech small caps gaining business traction and providing shareholder value. There’s no guarantee that these tech stocks will blossom into the next mega-cap winner, but all are contenders with at least a double-digit upside potential for their share prices.

Lightspeed Results and Repurchase Plan Lift Shares 20%

Lightspeed Commerce

(As of 05/16/2024 ET)

- 52-Week Range

- $12.23

▼

$21.71

- Price Target

- $18.47

Lightspeed NYSE: LSPD is a cloud-based SaaS that provides merchant and customer engagement services to small and medium-sized businesses. The platform resonates with clients. Clients are growing in number and deepening their use of services. The FQ4 results include a 25% increase in net revenue that outpaced the consensus estimate by 200 basis points on an increase in payment and transaction volume.

Other significant highlights include another quarter of adjusted operating profits, which made the first full year of profitability. The guidance is also favorable, indicating at least 20% growth in 2025 compared to the 23% forecast by the analysts’ consensus estimate.

Profitability is a key highlight. The company’s cash flow stabilizes, allowing the board to authorize a share repurchase plan. The plan aims to reduce the count by the maximum 10% TSX regulators allow and will likely continue in the following fiscal year. The post-release action is noteworthy because it lifted the market to the low end of the analysts’ target range, leaving ample upside for inventors. Analysts rate this stock as a Moderate Buy and see it advancing another 27% at the consensus midpoint.

Grab some Grab, The Super App for eCommerce

(As of 05/16/2024 ET)

- 52-Week Range

- $2.67

▼

$3.92

- Price Target

- $5.10

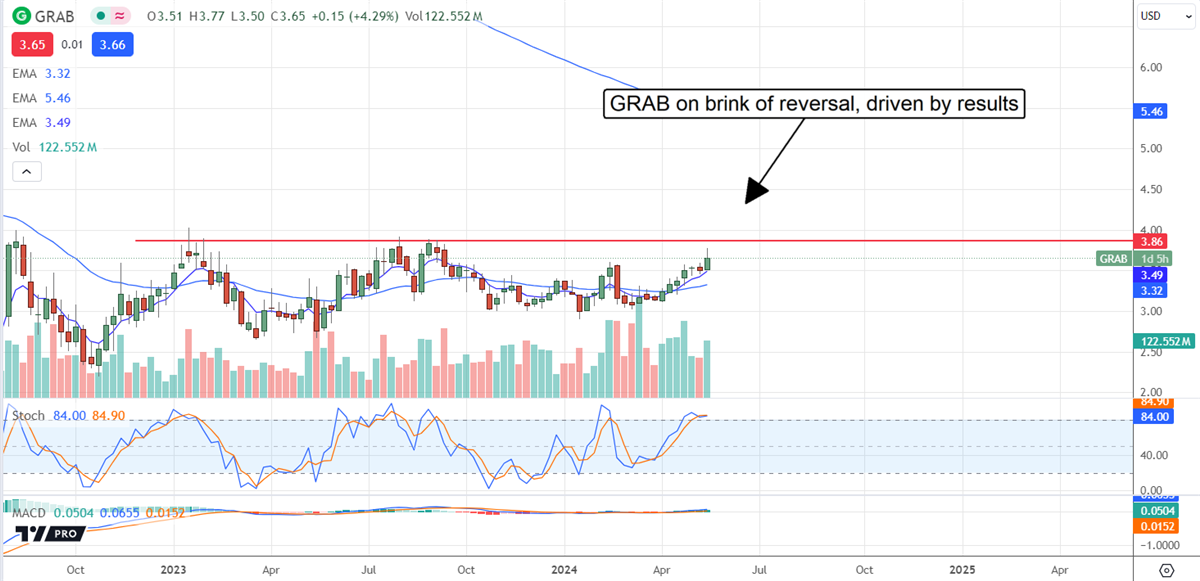

Grab NASDAQ: GRAB operates a platform for eCommerce spanning verticals and is known as a super-app. The company serves the Southeast Asian markets and is generally viewed as a deep value on the brink of sustained profitability with ample opportunity for growth. The latest results were mixed. Revenue grew 24% and outpaced the consensus, but earnings fell short. However, it is the outlook for profitability that has the market moving. The company reiterated its outlook for revenue while raising the range for adjusted EBITDA to above the previous.

The news is spurring the analyst to act. The first update tracked by Marketbeat is from Benchmark, reiterating a Buy rating and $6.00 price target. The buy rating aligns with the consensus of six analysts; the $6 price target is at the high end of the range and roughly 20% above the consensus target, which implies a 37% upside from current levels.

The technical action is favorable to investors and traders. The market is up more than 2.5% on the news and on the cusp of completing a reversal. The critical resistance is near $4.00 and may be reached soon. A move above that level would open the door for a sustainable rally to form. In that scenario, the market could reach the consensus target of $5.10 quickly, possibly before the end of the year.

Katapult is Ready to Launch, but Will it?

(As of 05/16/2024 ET)

- 52-Week Range

- $8.26

▼

$24.76

- Price Target

- $20.00

Katapult NASDAQ: KPLT operates a lease-to-own platform in the US. The share price dived in 2021 and hit new lows this year, but looks ready to start moving higher now. The FQ1 results include 18% top-line growth, better-than-expected GAAP losses, and favorable guidance for Q2. The company expects growth to continue in Q2 if at a slower 10% pace, supported by expanding the client base and growing share among existing merchants. That combination is expected to accelerate the top-line growth in the coming quarters.

Risks for this market include a lack of interest. There is only one analyst following it, Loop Capital and the last update is over six months old. The price target issued in September 2023 is $20, about 15% above the current action, but there is little to no market conviction to support it. Institutions own about 27%, suggesting a lack of conviction, and sellers outpace buyers this year. The market surged on the news but hit resistance above the $20 target and quickly reversed. The market now shows significant resistance that may not be broken without another solid catalyst.

Before you consider Grab, you’ll want to hear this.

MarketBeat keeps track of Wall Street’s top-rated and best performing research analysts and the stocks they recommend to their clients on a daily basis. MarketBeat has identified the five stocks that top analysts are quietly whispering to their clients to buy now before the broader market catches on… and Grab wasn’t on the list.

While Grab currently has a “Buy” rating among analysts, top-rated analysts believe these five stocks are better buys.

View The Five Stocks Here

Wondering what the next stocks will be that hit it big, with solid fundamentals? Click the link below to learn more about how your portfolio could bloom.

Get This Free Report